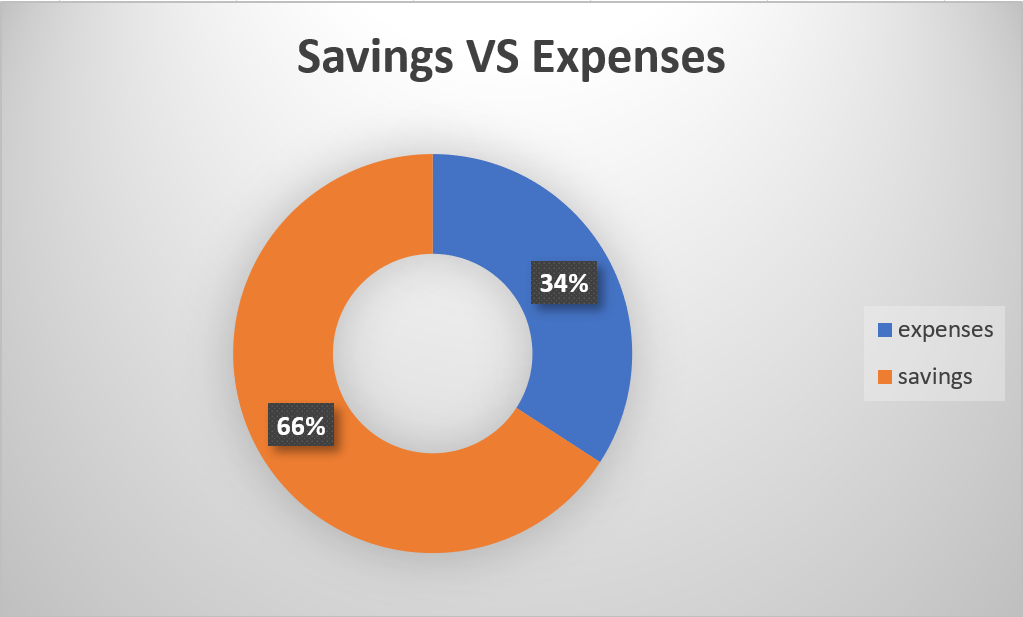

With the help of this article, you will learn a method to get an overview of your costs and to eliminate the hidden costs. I have saved about 60% of my potential income over a period of more than two years. Know your costs, that’s the main message. Some will say “I can’t save that much, I have to pay all that bills”. If your employer paid you 10% less, you certainly wouldn’t be sitting on the street under a bridge. You would suffer losses in your expenses, but your life would probably not change much.

Have fun, greetings from Germany.

We lose track of our money.

Nowadays, our money is mainly digital and we lose the track of its way. In past, we paid a lot with paper money and coins. It felt different to buy sports shoes for 200€ and have to take the money directly out of your wallet. Now it is simply paid with a single movement, be it a car or a chewing gum. The action is the same, you pay online or with your card. My 5-year-old godchild once said, he is already looking forward to finally having a smartphone, because he can then simply order all the toys. He doesn’t see the money that flows back and forth.

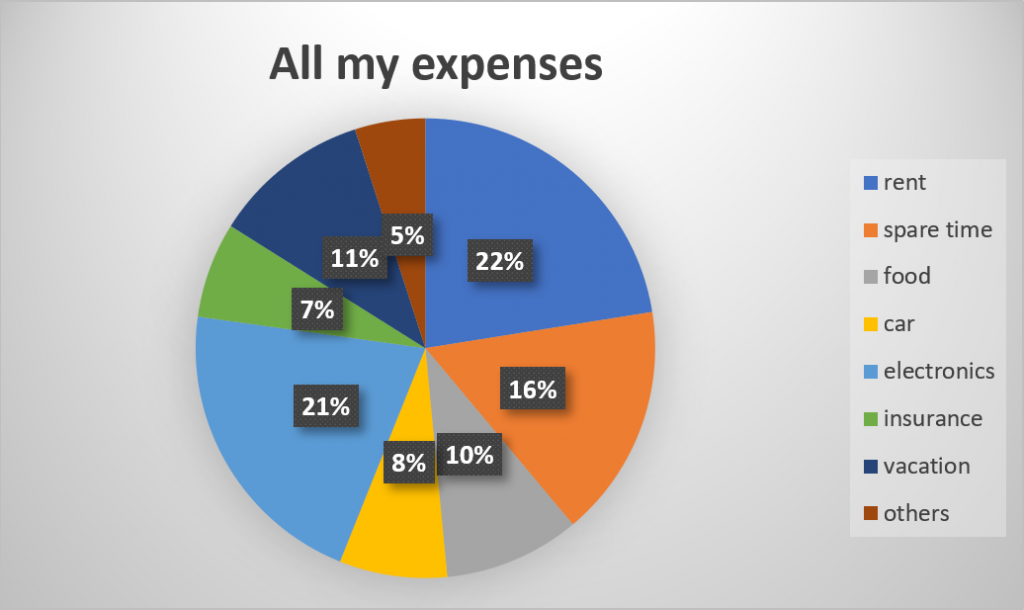

In order to counter this lack of transparency, I began to note all costs during my studies. I tried collecting receipts at the beginning, but I quickly switched to a financial app because I always had my smartphone with me anyway. This meant that the costs could be entered directly when they were incurred and evaluated at a later point in time. The following chart shows all my costs relative to each other. It concerns all costs this year from January to the day on which the article was published.

What does all this have to do with saving?

You can only save if you know where your money is going and which costs are fixed and which are variable. Spending €438.57 on games in 3 months is clearly too much. There were many small amounts in the course of the months, which add up, however, clearly reflected in the budget.

Many people say that they have too little money to save. Otherwise, they cannot satisfy all their needs. But most people here speak of demands and expenses without which they would not be more unhappy. Swapping a visit to the cinema for a nice walk saves money and is, in my opinion, just as beautiful.

So how do you get an overview of your spending?

The first step is to start. Enter as much as possible. Create a habit. Once this is integrated into life, the analysis can begin. I started it in the middle of my studies, it’s been three years now. Of course, it would have been better to start right before my studies in order to have a perfect evaluation of the whole time. But I’d rather just start instead of making excuses.

You can start entering costs that you have fixed every month as recurring costs. This only needs to be done once, and will from now on be taken over independently by the program. As a rule, the monthly rent does not change very often. The next step is to write down the daily expenses as efficiently as possible. Criteria are helpful in clustering costs. At the beginning I registered each bread of baker individually, today I enter the whole purchase as “basic supply” because it concerns only this information and their costs, not how many individual Croissants I ate.

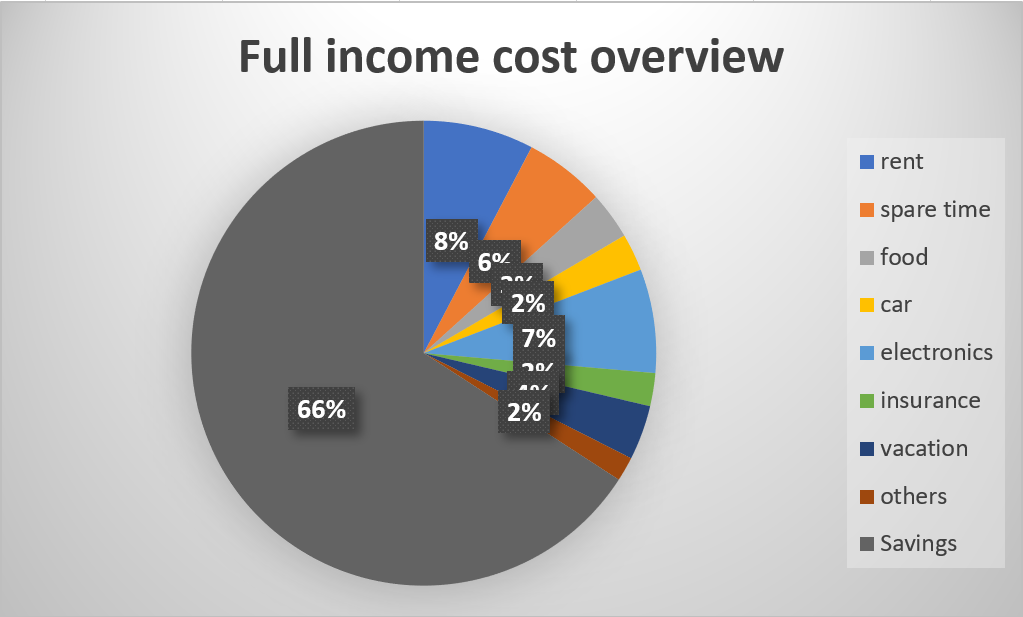

The recorded data can now be evaluated, relatively in my example. This is, of course, followed by absolute figures, but these are not relevant for this contribution.

Next are my categories, which have adapted optimally to my life in three years. They serve as a model and source of ideas, not as an absolutely perfect kind. Everyone should test them for themselves:

- Food and Beverages

- Electronics

- Car

- Vacation

- Free-time

- Apartment

- Clothes and shoes

- Assurance

- Health and body care

As an example of how categories can be broken down, I have once disclosed “Food and Beverages” here:

- Basic care (weekly buyings like milk, meat, water etc.)

- Lunch (food I need for life, but can’t do with weekly shopping)

- Snacks (Food I definitely don’t need, but who can resist chocolate 😀 )

- Going out in the evening (food that I definitely don’t need for survival, but fills my stomach and therefore would be wrong in the category “Leisure”. Nevertheless, it is good to have a separate overview of the rest of the meal. Depending on the quantity, there is a saving potential here per month. Or do you know from the moment you read this how much money you’ve spent on food this month?)

This structure allows you to show exactly where your money has gone at the end of a month. I’m amazed every month how much I spend on electronics compared to what I thought I spent on it. Men just love electrical things I guess 🙂

Key Takeaways

- In modern times, we are increasingly losing track of our money

- Just start writing down the costs, best of all via an app that allows you to evaluate directly

- Transparency reveals hidden costs

- Write down everything from the small ice cream to the new car purchase

- Numbers are better than feelings, they are more accurate

- Categories offer a good overview, with little effort

- Identify high expenditures and limit them consciously

Once you have collected some data about yourself, you can monitor your expenses and decide for yourself which were necessary and which were not. This way you can keep your expenses under control from month to month.

Have fun saving money! You are awesome!